Any man can become a father, but it takes someone special to be a dad! I was blessed with a wonderful childhood and could learn many financial lessons from my dad.

Since almost 10 years I’m now doing my best to be a dad myself. Being a dad is one of the most important jobs any man can have.

Becoming and being a dad got me thinking a lot about life and money lessons passed down to me so I can “pay it forward” to the next generation. Following one of my older posts about how to raise financially independent children and after quite some jacuzzi beerstorming, I’ve distilled the key lessons from my dad into 25 short but important lessons that lead to this blog post.

What Is The Job Of A Father?

First and foremost, kids should be prepared to stand on their own feet.

Beyond that, I believe good dads should try to give their kids both – roots and wings:

Roots to give them bearing and a sense of belonging.

Wings to help free them from constraints of any kind.

Thirdly, I appreciate that my father truly never told me how to live my life.

He simply lived his life and let me watch him do it.

Some parents worry that their children may not listen to them; I think they should rather worry that they’re always being watched instead!

As a great parent: You got to lead.

Live your life in an inspiring way.

This will set the bar for the next generation.

You’re the benchmark!

My Early Years

What is Money?

Since I can remember, money was always something mythical, powerful and highly interesting to me. As a young kid you watch your surroundings and learn from observing. It was interesting how this thing “money” could help my mum to buy so many groceries. It was interesting to see how we could get food at restaurants or fuel up the car with it.

Most transactions used this magical tool: Money.

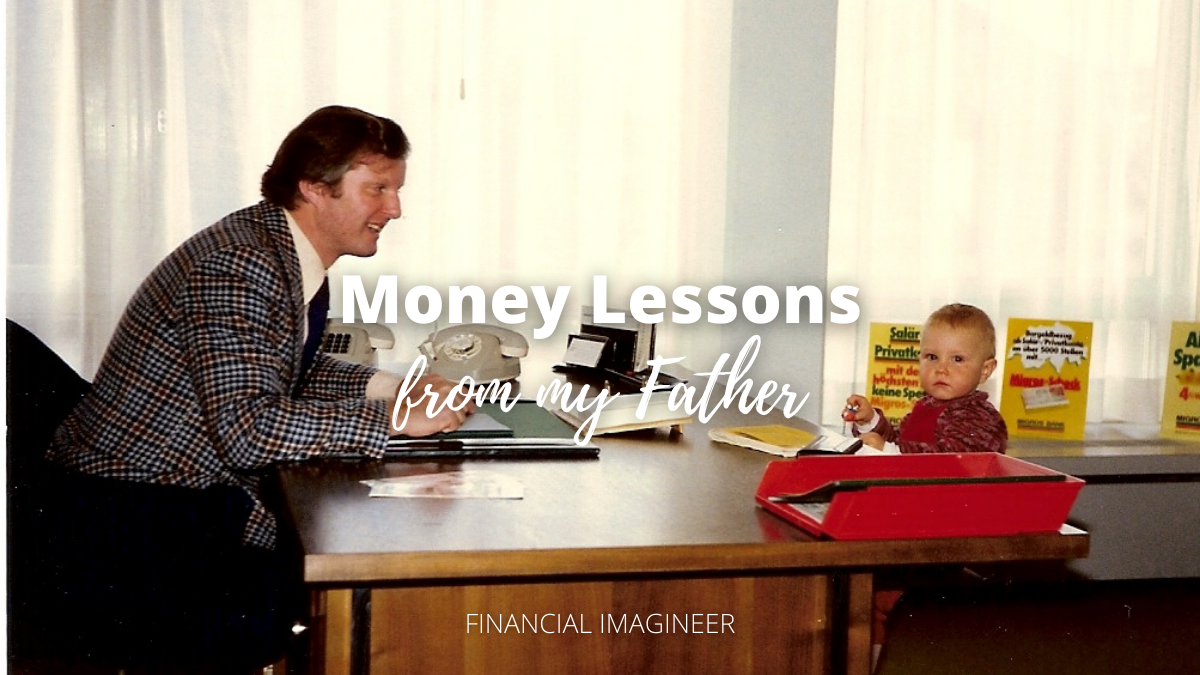

To my 4 year old brain the message was crystal clear: I had to figure out how to get some of this magical stuff myself! One day, my dad and I went to the city. It was the early 1980’s and one of the first ATMs got installed. My father brought me there to withdraw cash while holding me on his arms.

All of a sudden, money started coming out of a wall! The bills kept coming one after another back in the days. Finally I figured out where money comes from, from the banks of course! I asked my dad if I could take the next bill. He agreed.

I truly believed it was THAT easy back then. My dad quickly informed me that this is actually just his own money that he deposited at the bank earlier on.

Lesson 1:

Money doesn’t grow on trees: You got to work for it!

Lot’s to learn I still had.

After having understood this lesson, we – together with my sister and some neighbourhood children – started selling fruits and garden vegetables and more in our neighbourhood.

The level-up was to bring our old toys to flea markets and we started participating church sales as well.

Lesson 2:

Learn how to sell.

Make Money Visible

Have you ever heard a kid say: “I wish I could have a phone, so I could buy stuff.”

I’ve heard this in one form or another, and it triggered me deeply.

Spend money to buy something to spend more money?

Just think of it: Money today is mostly digital.

It’s a virtual thing.

Like coin points in Super Mario Brothers.

How can children learn lessons in this abstract world?

Many young people see money as limitless.

Money doesn’t seem to be really real for them anymore.

This is exactly why I let my kids see and feel money – and its consequences.

If kids are given financially relevant experiences in their life and someone is there to help them learn the lessons from those experiences, they have a higher likelihood of achieving financial success later in their life. They need to have them early and they need to have them often.

Mentor them.

It’s paramount to educate the next generation to make financial decisions. It will give them a head start in a world where money is largely a virtual illusion but has very, very real consequences.

As parents, we owe it to them to set them up for financial success.

How to?

Imagine, my dad once gave me a loan to satisfy my hunger for instant gratification. I was about 8 years young. I borrowed around $50 from my dad to buy a fluffy toy.

Oh boy, the sugar rush lasted less than a week.

We used to receive weekly allowances.

Every week my dad would take out a piece of paper where my negative position was mentioned. He would simply make it slightly “less negative” while my sister kept receiving her allowance.

It took me a few months to pay-off my fluffy-toy-loan.

The lesson stuck!

Lesson 3:

Give kids real money and life experiences. Let them feel the consequences of their decisions.

Papa-Bank

Now I’m the father and instead of allowances, I’m running Papa-Bank.

My kids can make deposits and each week they’ll receive a 1% payout.

This means for $100 in Papa-Bank the interest would be $1 per week. For $200 it’s $2 per week. Each week they can chose if they’d like to take the cash out or reinvest. I’ll hand the interest to them physically and let them decide.

Every. Single. Week.

Yes, it seems like I’m running a ponzi scheme here [potentially] as I can’t pay such high rates sustainably. But no worries, every once in a while, my kids will use some money to buy some things again.

That’s usually when they start to feel the impact of their decision as the weekly payouts shrink along as well. Sibling and rivalry with cousins is doing the rest.

Oh ya, before I forget:

Papa-Bank is only open for business with our family’s next generation blood relatives.

Papa-Bank also extended loans before. But instead of adding interest, I will take interest on that side. My son went through this experience already to until his nice elder cousin bailed him out.

Lesson 4:

Make money visible and talk about it openly.

Teenager Years

Nothing is Forever

In the early 1990’s Switzerland got hit by the real estate crisis. Suddenly home prices dropped 40-50% in value in just a few months. There where foreclosures and mortgage fallouts. Banks got hit. My dad lost his job during that time. Suddenly he was home. With us.

Lesson 5:

Life doesn’t always work out as planned.

When our dad started to be at home more, we initially got scared. I fondly remember how all of a sudden our family started discussing options to move to another city for work.

My sister and I didn’t like the idea of moving away from our home.

Lessons 6:

Include your kids in your life, discuss what you do, how you do it and why you do it.

Shortly thereafter, dad went hiking in the mountains for a few days.

By himself.

When he returned, he had a plan: He’s going independent!

It later turned out this was a blessing and the very best thing he could do – on so many fronts.

Lesson 7:

Take risks, never stop learning or trying new things.

From now on my dad wasn’t just at home in the early morning, late nights and weekend. He was there for us for most of our time. He was here to talk about life, school and more. He also started cooking for us.

Lesson 8:

The best gift and investment you can give your child is your time.

Zig Ziglar once said for kids “LOVE” is spelled T-I-M-E!

Kids will hopefully learn that having time with money is more valuable than having to go to work and spend your time earning money.

Introducing a Budget

We were like most teenagers and suddenly got a taste for fancy sneakers, expensive hoodies and other branded stuff. We were not told off. My sister and me each had a “clothes-envelope” at home.

Each month my father would pay around $50 into the envelope and keep a balance sheet. We were free to use the contents to purchase clothes, shoes or pay for haircuts.

This was our pre-paid necessities budget.

Lesson 9:

Have a budget.

Looking back it’s a great way to make money available and visible without imposing potential arbitrary invisible barriers as to what is good and what is bad to use it on. It was clear: If we saved-up we could purchase the more expensive things. But we had to be patient.

The decision, the marshmallow test and trade-off has all been delegated to us kids.

No more instant gratification.

We had to learn it ourselves.

Lesson 10:

Marshmallow test your kids frequently and in different ways.

Learning to Help Myself

As a 13-year-old, the greatest dream I had was to have my own TV. In my bedroom. When I first mentioned this idea to my parents, my mum was fully against it while my dad simply said: “Yes, why not – but you got to earn it yourself.”

I learned that from age 14 onwards it was possible for me to become a newspaper boy. I applied immediately and got a paper-route with 400 households to serve. When I turned 14 my days changed. No matter the weather, if sunshine, snow, rain, storm, heat or cold, I had to serve my 400 households or face losing my job.

That job earned me $500/ month.

A very decent pocket-money for a 14-year-old in the early 1990’s.

Lesson 11:

Understand your kids motivations and let them go after their dreams.

After three months, I had sufficient cash aside to buy the TV. Once I got paid I rushed to the shop and bought the largest 16:9 TV available back then. It was a monster. I couldn’t transport it back home. That’s why I called my dad and told him what I just bought.

He simply said: “Oh, you actually did it. Wait, I’ll be on my way.”

A few weeks later I was enjoying my TV a lot but started to realize my bank account was almost back to zero once again while my time invested distributing all those newspapers is gone forever.

This is what motivated me to get started saving ultimately.

When kids are given the opportunity to engage in strategically relevant experiences and given the ability to learn the lessons from these experiences, will have a higher likelihood of success in their life.

Lesson 12:

Don’t just “go” through life, grow through it!

First Investment Experiences

When I was 16 years old I got a special gift for Christmas: My dad prepared an investment account with one share inside for me. Again, instead of telling me what to do and what not to do, he simply said:

“Let me know when you have any questions.”

I was bloody excited and started reading up on investing instantly. It’s amazing how this motivated me to read. Soon thereafter one of my all-time favourite books came to the market: “Rich Dad. Poor Dad.” by Robert Kiyosaki. While it has nothing to do directly with investing in stocks, it kicked-off my money book library in 1997.

The markets where exciting. Soon the new economy boom started going into overdrive. Sure enough I put the largest amount of my portfolio in Dot.com shares. They were on FIRE. By 1999 my portfolio grew nicely. Also in 1999 everyone thought Warren Buffett is too old to still be relevant.

As the markets kept climbing higher, I sold some stocks and bought a fancy second-hand sports car.

I sold more stocks to finance an apartment where I moved in with my girlfriend at 19.

Lesson 13:

Avoid lifestyle inflation.

Soon thereafter the market crashed.

My portfolio was suddenly back to square one again.

In total, it took me 5 years before I took my dad’s offer and went back to him with my first questions!

He laughed and uttered:

“Wow, that took longer than I thought.”

Do I regret going to him earlier?

No. No regrets at all.

Lesson 14:

Making mistakes and learning your lessons early in life is more valuable than just reading books.

This lesson is one of the most valuable in my view.

You see, indirectly my dad encouraged me to take ownership and fail early.

Once I understood this lesson in retrospect, it changed my mindset completely. Failure is NOT the outcome of your immediate actions.

Failure is not even trying.

Failure is standing still.

The biggest failure is not learning your lessons and trying again.

In our schools you might still get punished to make mistakes. That’s why in our society we’re afraid of trying and failing. Hence, many don’t even try anything anymore!

In our family, I’d be disappointed if my kids are not trying and failing at something every once in a while.

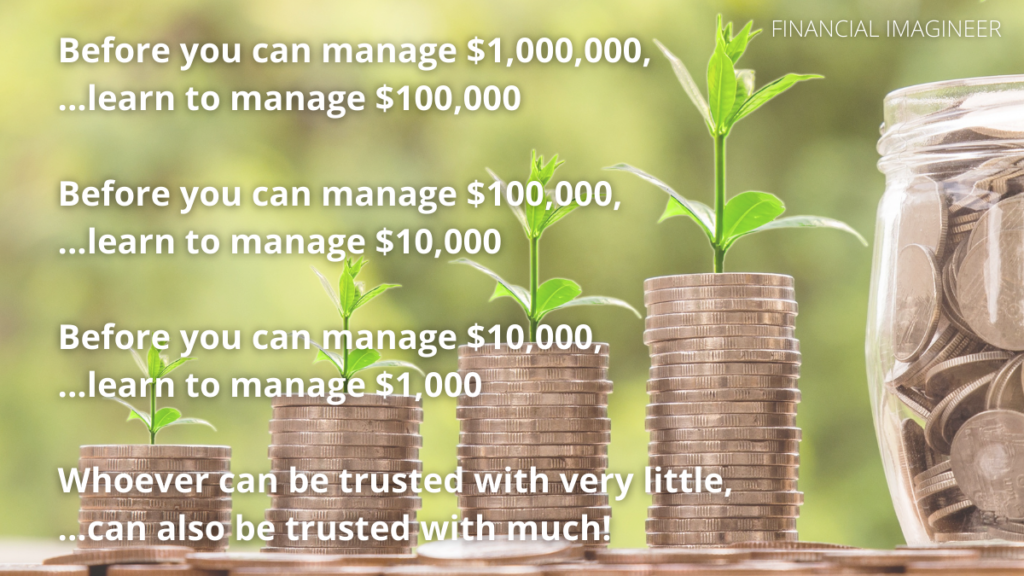

Lesson 15:

Whoever can be trusted with very little can also be trusted with much.

Young Adult

When we were in our teenage years, my dad kept telling us two things

1. He’d like us to move out before we reach 25 years of age.

2. We would always be welcome at home – in case we truly need help.

As written above, this motivated me to move out of my parents home at age 19 – I was a University freshman.

It also motivated me to hustle all kind of jobs. I worked part time as a bank teller on Saturdays, delivered pizza and later moved up to manage a pizza delivery business part-time as pizzajolo baking up to 200 pizzas per night regularly. It also brought me to work at the polling office of our community.

Due to all these activities I had a decent $1,500 – $2,000 per month salary as young student.

Lesson 16:

Learn how to stand on your own feet early.

Thanks to my previous mistake of investing in high octane tech stocks only, I reconsidered my approach and started funding a monthly mutual fund savings plan. At first I fed it with about $300 per month but during some frugal months I managed to stash more then $1,000 per month as well.

Thanks to the lessons learnt, the pot started growing again.

Lesson 17:

Make a mistake once and it becomes a lesson. Make a mistake twice and it becomes a choice.

One evening in my most crazy side-hustling days back in 2001, I was watching “Who Want’s to be a Millionaire” on Swiss TV3. It was boring, none of the contestants seemed to make it past some simple questions.

This motivated me to write them a complaint letter.

Read here about how this has turned out for me.

Lesson 18:

Luck is when preparation meets opportunity.

With a six-figure bank account at 21 – I was free to explore the world.

I chose to invest in my skills, learned Spanish and Mandarin Chinese. Ultimately, I ended up in Taiwan where it got really adventurous: I lost my job and working permit in Taiwan due to signing up with the wrong company…

When I called my dad back in 2004 to report to him what happened he answered the phone and replied:

“Welcome to life.”

I enjoyed that reply so much.

We laughed.

It encouraged me to stay the course.

Lesson 19:

A smooth sea never made a skilled sailor.

Together with my girlfriend’s – now wife – help we managed to find me a second job in Taiwan. More about this story and how we planned our future together can be found in my guest post for JD Roth’s Get Rich Slowly.

Lesson 20:

Failing to plan is planning to fail.

Middle Age

It was the year 2015: On my 36th birthday, my dad gave me a very memorable phone call. In retrospect I could say this was probably the most valuable birthday gift I’ve ever gotten.

That’s why I’d like to share it here.

In 2015 my dad was 72 years old, I turned 36… he was exactly double my age!

I picked the phone.

My dad started: “Happy Birthday Son! You’re now already half my age!”

He went on: “You’re catching-up!”

And finished with: “Beware, the second half goes faster!”

This call stuck!

Three facts of life served up.

It got me thinking very, very deep in the days, weeks and months to come!

Lesson 21:

Time flies! Winter is Coming!

My thoughts where all about the value of time in life.

Read: Your Money or Your Life!

When you’re young, you got all the time in the world and it seems to be a reasonably fair thing to sell some of your time against some money to make a living. As you grow older, your reservoir of remaining “life-time” shrinks and in turn the remainder of your days keeps going higher in perceived value – to yourself and others. The older you get, the more it hurts if you still must sell your time for money…

Lesson 22:

Everything is about supply and demand. Everything!

During my career as Wealth Manager I was helping millionaires with their investments. Thanks to great guidance and working with inspiring people I’ve learned reasonably well how to invest and make money work for us by age 36. I’m so nerdy that I’ve actually kept a spreadsheet with all our assets, liabilities, income and expenses since the late 1990’s – it got a yearly update!

After listening to my dad’s voice about the speed of time, we started playing through some scenarios in my spreadsheet and identified two key areas for optimization:

- Generate passive income to cover our family expenses

- Activate “passive” assets and optimize our income/ expenses

Since our 5-year plan was due for discussion in 2016 I’ve added some new dream goals till 2021:

- Retire from my 9-5

- Start my own blog and business

Yes, one idea was to potentially let go of my job.

My dad used to say that each job is like a three-legged stool.

The three legs are:

- What you do

- What you get for it

- With whom you do it

As long as at least two of these legs are still working out for you. You’ll stay.

Also, everything is subjective. Priorities in life change.

We became parents and where looking for more time flexibility.

And maybe I was also looking for a new challenge.

Lesson 23:

You know that you’re on the right path whenever you feel things stop being easy.

This lesson is very close to my heart. Basically, it’s like if you think of playing Mario Kart on “easy”: You’ll always win. As you advance through life, also adjust the level of difficulty gradually.

After 2015 I started reading more into the FIRE concept and idea!

That’s when I suddenly read Mr. Money Mustache’s “The Shockingly Simple Math Behind Early Retirement“.

However, I’ve had some concerns about the “RE” (retire early) part:

- Don’t retire from something, retire TO something.

- Have something to do, someone to love and something to look forward to in life.

- Instead of being idle, try to find and live your “Ikigai”: Live a purposeful life.

It turned out my “RE” was more a “Retire to Entrepreneurship” – you could also name it “Recreational Employment” if you will.

Another deep concern was the kind of role-model I want to be for my kids.

- concern of my kids not seeing me work anymore

- live the life you want your kids to be inspired by

Whatever you plan in your life: Be a role-model for your kids.

Kids don’t quite “listen” and “follow your instructions” about living life – they rather watch how their rolemodels [hopefully their parents, make them chose YOU] live – and learn by watching!

To achieve this, be an inspirational role-model and ensure your lifestyle ticks all the boxes of lessons you want them to learn and absorb. Chase your dreams while they can watch and learn is the best starting point to set them for a happy and successful life.

Lesson 24:

Don’t tell your kids how to live their life, live yours, and let them watch!

Work is not just a 9-5-working-at-something, it can be anything – as long as you work hard towards achieving whatever goal you’ve set yourself.

Let your kids see you succeed AND fail.

This is YOUR chance not to raise “next-gen-rat-racers” or “trust fund babies” that will venture out to live an ordinary life – let them learn from you how to life an extraordinary life instead!

By mid-2017 we’ve set-up sufficient monthly recurring passive income streams from different sources and worked out a plan that allowed me to quit my 9-5.

We FIREd.

Lesson 25:

Live like a role model – work hard to chase your dreams to set an example for kids to inspire them to work hard on achieving their dreams later.

Invest in your dreams!

What advice would you give your younger self?

What lessons did you learn from your family?

“Life” is a gift to you. The way you live your life is your gift to those who come after.

Make it a fantastic one.

Matt

Disclaimer: Please be made aware that the some of the links used above may be affiliate links for which Financial Imagineer could receive a compensation.

Great post! I think those are all awesome actionable teaching points for kids. Going to start with my one year old today! ?

My dad was a great role model, he only made middle class pay but he invested well and became a millionaire, and in fact bequeathed a million each to my brother and me. But he worked for a corporation his whole life, as did my brother and I. We both retired early, but only slightly early. I found the corporate life to be exciting and purposeful. I was much happier than my friends who ran their own businesses, still am because I’m happily retired, consulting a little, and they can’t find an escape plan from their family businesses. I don’t think either path is always the best, but neither is always the worst either.

You were blessed to grow up in a world where money wasn’t taboo!

It’s a great collection of lessons and a mindset I strive to pass on to my children.

Pingback: Thursday’s Top Three (TTT #009) – Money Savvy Ladies