Money has been around for a long time. Its evolution is a process that will continue indefinitely and will be shaped by the constantly changing needs of its users.

The evolution of money has been a long process. It started out as bartering and evolved into coins which were made of precious metals like gold, silver or copper.

Paper money came about in the 18th century when economies became more sophisticated and was backed by gold reserves.

In this blog post, we will discuss the evolution of money from trading goods to digital currencies that are being experimented with now and will try to show the most likely next upcoming steps investors might want to consider.

Money is one of the most important inventions in human history and has always been an essential part of our evolution as a society.

1. What is Money?

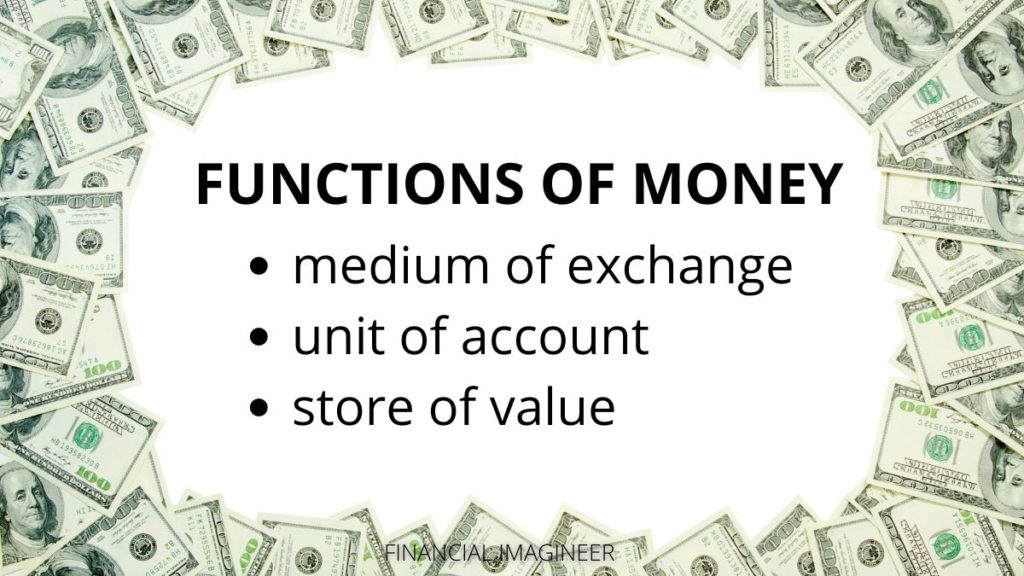

Money is one of humanity’s most important inventions and usually serves three main functions:

- medium of exchange

- unit of account/ form of measurement

- store of value/ human achievement

The introduction of money for trading purposes made valuation easier and facilitated trading and storage of values efficiently over time.

Money can be anything that has a unit of value and can be used to pay for items or services. Money helps us transact, measure achievements as well as safeguard them over time.

2. The Ongoing Evolution of Money

The evolution of money has been ongoing for millenia.

It will never stop.

Money will change as societies evolve and adapt to their evolving needs.

Money has evolved many times throughout history. It started out as bartering, then coins were made of precious metals like gold or silver and paper money came about in the 18th century when economies became more sophisticated.

In the early 21st century, fiat currencies are issued and regulated by central banks, they used to be backed by gold or other precious resources but this backing got removed back in 1971 when the Bretton Woods agreement was uplifted. New forms of currencies such as central bank digital currencies and cryptocurrencies backed by an innovative blockchain technology are starting to gain ground and have opened up an entire universe of new opportunities for investors.

“Ignoring technological change in a financial system based upon technology is like a mouse starving to death because someone moved their cheese.”

Chris Skinner

While fiat paper cash may still be what people use most often in their daily lives today, there’s no doubt that digital transactions will continue to grow over time as cryptocurrencies allow secure peer-to-peer exchange without involving financial institutions or central authorities while also making micropayments much easier thanks to lower fees compared to credit cards or traditional wire transfers.

We are once again at a crossroads of monetary evolution:

New forms of money are being invented and experimented with.

All it takes for a new form of money to emerge and catch on is a group of people who believe in its value and use it for their transactions.

In short: It needs broad acceptance by a majority of society.

For now, we are still in a period of uncertainty as to what will happen next. We are facing an evolution that is changing the entire financial landscape as we know it and entering uncharted territory.

While central banks have been struggling with their decisions to issue any new and updated currencies, cryptocurrencies like Bitcoin or Ethereum have taken up speed for now since they offer a lot.

However, the race for the next evolutionary step forward is wide open.

Trust in the process!

3. New Money

Currently there are three main types of money being in circulation at the same time: Fiat currency (such as the US dollar, the EUR or the JPY) which is regulated by governments around the world; central bank digital currencies or CBDC (central banks controlled and issued, no physical backing) and cryptocurrencies such as Bitcoin or Ethereum that are blockchain based and largely unregulated.

There have been many forms of money throughout its evolution, new forms will keep coming up while others will eventually fade away once there is not enough demand from users anymore.

We are at such an evolutionary crossroads at the moment: The new dominant next generation form of money might be chosen within the next few years.

“Banking and money has to work when and where you need it. The best advice and the best service in financial services happens in real-time and is based on customer behaviour, using principles of Big Data, mobility and gamification.”

Brett King

What is a FIAT Currency?

Fiat currency is defined as a form of money that has value only because it is declared legal tender by a governing body.

Pros and cons of FIAT money

Pros:

- stability

- sense of security

- regulatory framework

- general broad acceptance

Cons:

- issued and controlled by central banks and governments

- usually value inflates away over time, unlimited printing possible

- no transparency, black box

- high fees for international transfers

What are central bank digital currencies or CBDC?

Central Bank Digital Currencies, also known as CBDCs, are digital currencies issued and controlled by governments/central banks. They can be exchanged electronically with transactions being recorded but no physical cash will ever change hands.

Central bank digital currencies or CBDCs are different from cryptocurrencies because they are issued by central banks and controlled/regulated by the government. Cryptocurrencies are fully decentralized and use the blockchain technology whereby CBDCs are fully controlled by an authority.

The evolution from fiat paper cash to central bank digital currencies might happen pretty soon if enough people start using them.

Pros and cons of CBDCs

Pros:

- similar list of pros like for FIAT money

- one way to include new technological advances while retaining control

- lower volatility then uncontrolled digital currencies or crypto solutions

- regulatory framework even stronger as with FIAT, total control possible

Cons:

- issued and controlled by central banks and governments

- new solution, kind of a hybrid between FIAT and crypto

- trust of broad population would have to be won over first

- no transparency, black box

What are Cryptocurrencies?

Cryptocurrencies are digital currencies that use cryptography to secure transactions and control the creation of new units.

They provide a decentralized alternative for central bank issued fiat or digital currencies: They work on peer-to-peer protocols which means they don’t require any intermediaries (no banks, no credit card companies). Value transfer is fast due to low transaction fees.

There has been an evolution process in cryptocurrencies since Satoshi Nakamoto created Bitcoin back in 2008 but only recently have there been many other major evolutions with Ethereum’s smart contracts being one example or Monero offering more privacy/anonymity compared to Bitcoins for instance.

The money YOU choose should depend on your needs and your personal preferences. Evolution will prevail and money will keep evolving further anyways. It’s like a very healthy competition for the best possible solution to solve our need for a form of measurement, exchange and storage of value.

Pros and cons of crypto currencies

Pros:

- totally independent, decentralized currency system

- high security standards and high transparency with the blockchain

- instant and cheap transfers 1:1 transfers possible, no intermediary needed

- allow for most technological advances to be used

Cons:

- remaining uncertainty about governments and controlling organs

- extremely high volatility make it less interesting for people looking for stability

- allows to circumvent money laundry and other fences installed by regulators

- trust of broad population has to be won over still

“We’re witnessing the creative destruction of financial services, rearranging itself around the consumer. Who does this in the most relevant, exciting way using data and digital, wins!”

Arvind Sankaran

4. Implications of Monetary Evolution for Investors

As a daily user of “money”, as investor, as participant of our global economy, your primary goal is to keep track of value and hopefully increase your purchasing power over time.

In the end it’s all about staying up to date, open-minded, and adaptable to change. This is how you may get the most out of your investments over time. Keep the flexibility to adjust quickly when market conditions change or new opportunities emerge – as a result of evolution.

If cryptocurrencies become more popular in the future, prices are going to rise. This will be a highly interesting opportunity for short-term investors. However, this kind of betting on the next best thing could also turn into gambling if not enough research has been conducted before putting money at stake. We all do not have a crystal ball.

So, let’s try to focus on what we know:

Fiat currencies have always lost value throughout history because they are printed constantly with no physical backing (which again is the main reason why central banks keep printing them). Fiat currencies only work as long as people believe they do so inflationary trends should be monitored closely – this much is for sure!

However, we also know that governments and institutions will try everything to ensure monetary control, as controlling money is power.

It will be very interesting to see if FIAT currencies or cryptocurrencies have a stronger hold in the future. While cryptocurrencies seem to be much more independent at the moment they could become heavily regulated because not doing so would surrender control and power.

In this area, central bank digital currencies would clearly win as they allow for total control over money flow and transactions while still allowing for new technologies to be used.

“Financial institutions must be able to deliver an easy to navigate, a seamless digital platform that goes far beyond a miniaturized online banking offering.”

Jim Marous

5. How to Participate from Monetary Evolution?

Usually shifts of that seismic magnitude don’t just happen overnight so if you keep track of how money as such evolves, you can try to take advantage of each step by investing accordingly.

What does this mean?

It implies that while no one has a crystal ball, but focusing on what we do know can help us make educated decisions.

Take into consideration your risk tolerance and investment horizon though!

After brainstorming this situation with friends and experts, I like to compare the current situation with the time before the new economy bubble in the late 1990’s: Back then everyone kind of knew the internet and the “New Economy” is going to be the next big thing. However, just nobody had a clue on how exactly this revolution is going to unfold. In 1998-99 everyone jumped onto the internet bandwagon by buying “dot com” stocks – until they crashed very badly and led us into a recession. Only in the aftermath of that crisis did a few selected winners emerge from the ashes.

“By lowering the barrier to create new digital currencies and applications, we will see an explosion in the numbers of ideas tried.”

Brian Armstrong

Prior to the “New Economy” crash there were so many small companies that went IPO and later on disappeared again. Ultimately, the big winners emerging from the ashes were not necessarily Yahoo, AOL or any of the big names who appeared to be winning prior to the crash.

Similiarly, we might be facing some kind of “washout phase” ahead of us before the final winning players are gonna be known. Such an event would be an awesome moment to get into the game for anyone who is not exposed yet.

Just imagine you bought Amazon back in 2001.

Focus on what you know!

For now, we do know:

- FIAT currencies do have inflationary tendencies

- most central banks have issued incredible amounts of liquidity into the system

- central banks are highly indebted and might not be able to repay all debt

- central banks and global institutions will try everything to secure power over the monetary system

If you “align” yourself with central banks, you’ll be on the winning side no matter what.

How to align?

Expand your own balance sheet, have a comfortable level of “good” debt outstanding (do NOT overleverage beyond your comfort zone!) and hold assets against it.

Another way would be to hold some cryptocurrencies such as Bitcoin or Ethereum but please do try to avoid the so called shitcoins. These will be the ones washed away once the time has come to crown the final winner here.

Conclusion

The evolution of money is a highly fascinating topic and there are many different areas to take into consideration. From cryptocurrencies like Bitcoin and Ethereum, to central bank digital currencies that may one day be the norm even to ideas that we might even not be able to comprehend yet.

“Banks have to upgrade themselves, or risk being burnt to the ground.”

JP Nicols

There will always be pros and cons for each type as well as dangers and opportunities.

One thing is clear, one day in the future there will be a day where a new form of money, or a new lead-currency will be globally accepted and this will impact anyone using money on this planet – you, me, all of us.

If you enjoyed this post, you will love reading my blog post “The Bitcoin Millionaire” to understand more details of how to think about Bitcoin in particular.

The information shared in this blog post is no investment advice and should help you get started thinking about how you could prepare to participate from ongoing monetary evolution. Consider your risk tolerance and investment horizon which will depend on what stage of life you’re currently at!

“Technological innovations will be the heart and blood of the banking industry [and money] for many years to come and if big banks do not make the most of it, the new players from Fin-Tech and large technology companies surely will.”

David M. Brear

If you want to learn more about money skills, read more here or join my free online webinar here.

If all of this sounds too complicated or intimidating and you would like help or brainstorm some ideas with me, please do feel free to book a free of charge 30 mins consultancy session with me.

I sincerely hope this blog post was helpful for you!

“At the end of the day, customer-centric fin-tech solutions are going to win.”

Giles Sutherland

In the meantime, please do let me know what your plan of action will be with regards to monetary evolution in the comments below.

If you like what you read, please consider subscribing my blog by email below and follow me on Twitter or Facebook.

Have a rich day!

Matt

This is more helpful than the evolution of money I took in my history class. It’s WAY more detailed. Thanks for sharing!

Thanks for stopping by Vishnu, appreciate your comment and happy to have helped understanding money evolution better!

its total madness how the overwhelming majority of people on the street have no idea how money is created!